Preliminary December data from local real estate boards – released after our latest housing projection – suggests some better than anticipated momentum in housing at the end of last year. That said, one must be cautious in drawing too many conclusions from December data, as its typically a low volume sales month, and unseasonably warm weather may have pulled forward purchases. More broadly, the drops registered in Canadian home sales and average home prices in 2023Q4 overall were generally as anticipated.

Our updated forecast calls for a gain in Canadian home sales in 2024Q1, compared to the small decline we had previously expected (Chart 1). This increase reflects a downwardly revised near-term profile for borrowing rates, a resilient job market, and the release of pent-up demand. On the latter point, we estimate that sales had undershot levels consistent with fundamentals like income, population growth and supply by about 15% in the fourth quarter. Canadian home sales should also receive an important boost from Bank of Canada rate cuts (see forecast), supporting rising sales activity through the year.

Improving sales activity will likely not be enough to stem a first quarter decline in Canadian average home prices, given the relatively loose supply/demand conditions that are likely to prevail, on balance. National prices should flatten out in the second quarter before rising through the rest of 2024 and 2025, though the pace of increase will be restrained by challenging affordability conditions in several markets. Underpinning this view is our expectation that listings will remain relatively subdued over the next few years, with economic uncertainty keeping would-be sellers on the sidelines in the near-term, and a resilient jobs market keeping listings from spiking higher over the projection horizon.

The regional disparities that charactered markets in recent quarters are anticipated to persist. Over the next few years, we see price growth outperforming in the Prairies, supported by solid affordability conditions, tight markets, and economic outperformance. Alberta’s market continues to draw strength from the fastest population growth in the country. Elsewhere, tight supply/demand balances should keep near-term price declines muted in Quebec and the Atlantic before tough affordability conditions limit price growth to a below-trend pace thereafter.

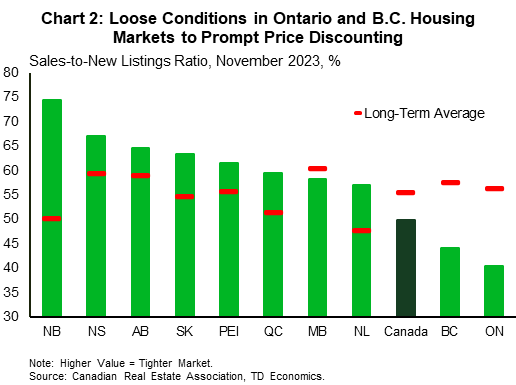

In contrast, within Ontario and B.C., supply/demand balances indicate that conditions are loose compared to historical norms (Chart 2). As such, price discounting is likely on tap over the next few months before the supportive factors outlined above yield second half gains. We expect quarterly sales growth to be the strongest in these two markets through the projection horizon, which will support prices. However, a depressed starting point is a big part of the story (per capita sales levels were about 30% below long-term averages in both markets during November). Sales should remain low in B.C. and Ontario moving forward, holding below their pre-pandemic levels into 2025.

Downside risks are consistent with what we flagged in our prior projection, in that economic growth could be weaker-than-expected, or the Bank of Canada may be forced to hold their policy rate higher for longer than we anticipate, should inflation remain higher-than-expected. However, upside risks to the projection have come into fuller view. Bank of Canada rate cuts (and the signaling that precedes them) will likely jolt market psychology and could cause sales and prices to rise by more than we anticipate in the quarter they are initiated (and perhaps even before).